- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

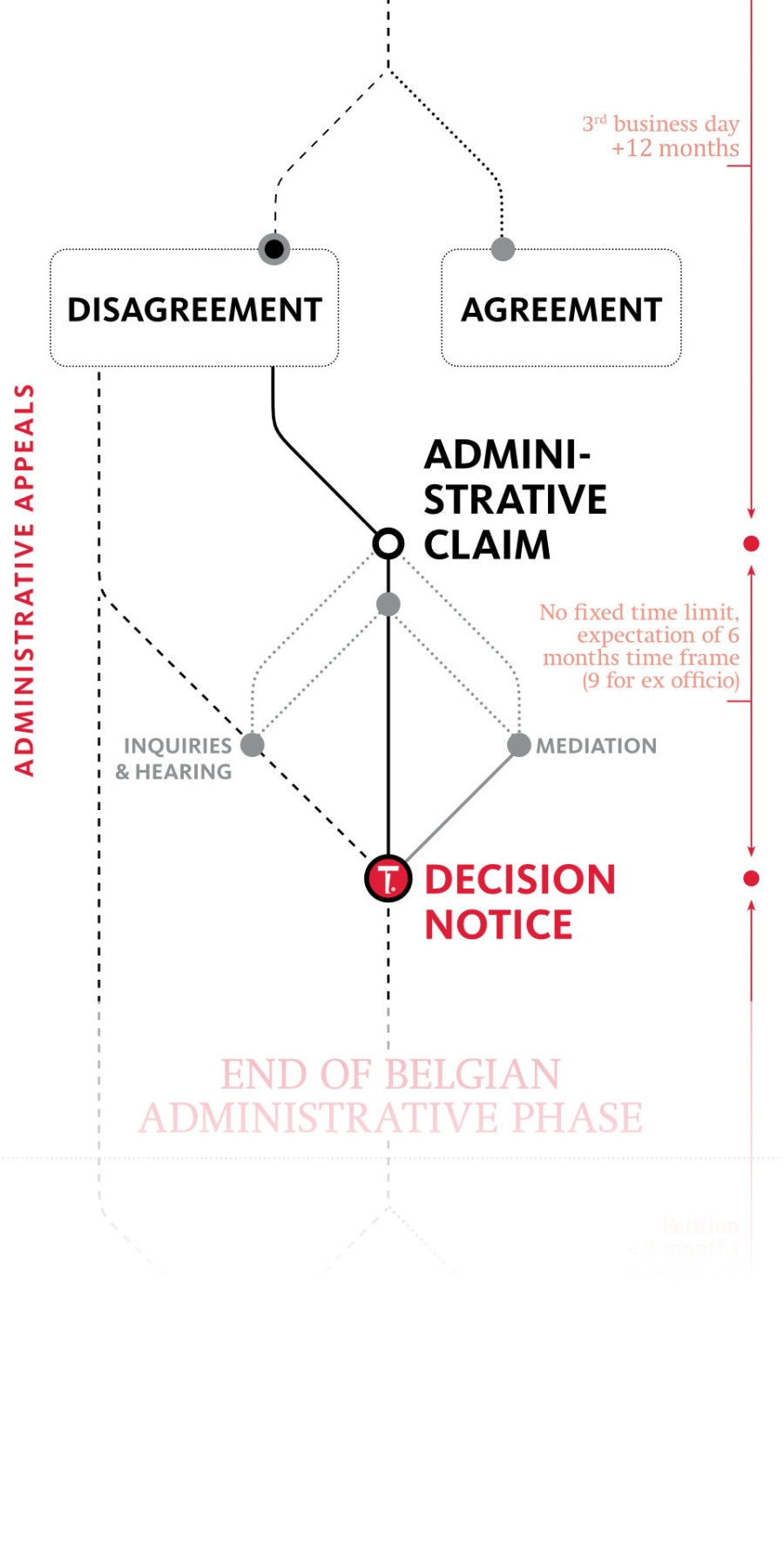

Upon receipt of an additional tax bill, taxpayers have in principle 1 year to file an Administrative Claim. This initiates the administrative appeal phase which must be exhausted by the taxpayer before initiating the judicial phase. The file accordingly will be handled by the Regional Director who will review the position of the tax inspector that has performed the audit and has concluded on issuing the tax bill.

Once the tax bill has been received, the taxpayer has 1 year to file an Administrative Claim (“Bezwaarschrift” / “Réclamation”) vis-à-vis the Regional Director of the General Administration of Taxes. The period to lodge an Administrative Claim on paper starts on the third day following the date of sending the tax bill, and the lodge an Administrative Claim by electronic means, as from the day the tax bill is made available via eBox and MyMinFin.

Considering the impact of interest on the tax liability it should be assessed whether one should use the full extent of this timeframe or act more swiftly. It is recommended to file the Administrative Claim within the period of 2 months (i.e. the term of payment) when the taxpayer decides not to pay the tax bill (after the 2-month period, the tax debt will be due and can be collected by the competent tax receiver in case of no Administrative Claim).

The Administrative Claim initiates the administrative appeal phase, which aims to resolve tax disputes, without litigation. This administrative appeal phase is a mandatory first step for the taxpayer to take since lodging an application to the Court of First Instance, the initial step in the judicial phase, is only allowed when the administrative phase has been exhausted.

Notwithstanding the fact that the taxpayer has a strict time limit of 1 year to lodge the administrative appeal, the Regional Director is not bound by any time limit to issue a Decision Notice (“directoriale beslissing” / “décision directoriale”). If, however, such decision is not made within a timeframe of 1 year (or 9 months for ex officio assessments), the administrative phase is deemed to be exhausted and a taxpayer may file for a petition with the Court of First Instance.

As with the taxpayer’s reply to the Rectification Notice, the Administrative Claim should be well thought through whereby it is important to note that the addressee of the Administrative Claim is different – i.e. the Regional Director and not the tax inspector that has performed the audit and issued the tax bill. Because of the Administrative Claim, the Regional Director is to perform an internal review to (re-)consider the position of the tax inspector.

Therefore, the Administrative Claim should focus on the specific grounds for the objection for the Regional Director to primarily understand the facts and the legal position. The arguments put forth in the reply to the Rectification Notice may be referenced to and potentially supplemented by additional argumentation. Finally, the taxpayer’s assessment of and critique on the tax inspector’s motivation as laid down in the Taxation Notice could form a substantive part of the Administrative Claim. As such, the principles of good administration (legal certainty, proportionality, etc.) can play an important role in the (internal) assessment of the Regional Director, who can autonomously organize further investigations.

It should be noted that an Administrative Claim can only be filed by the taxpayer on whom the tax is imposed, or (if applicable) the successor to the rights and liabilities of that taxpayer, or a legal representative acting on behalf of such taxpayer. Notwithstanding attorneys-at-law’s monopoly to plead in court and their ‘mandate ad litem’ only applies to the judicial phase, the involvement of the attorney-at-law, in our view, can be of strategic importance already in the administrative phase and certainly in view of later proceedings in the judicial phase (when applicable). In this perspective it should be noted that the Regional Director may be more sensitive to other parameters for deciding to pursue the judicial phase than the tax inspector would take into account – including a.o. assessing chances of judicial success and spill-over risks in terms of jurisprudence. Being knowledgeable of the file being handled by an attorney-at-law at the administrative phase may shed a different perspective on the assessment of the Regional Director to appreciate the strength of the tax inspector’s position and case built against the taxpayer vis-à-vis that of the taxpayer being represented by an attorney-at-law who can deal with the next phase as well (unlike other tax consultants that do not have the possibility to plead before courts). A key aspect of the Administrative Claim, finally, is to request a review (on location) of the file of the tax inspector and to request to be heard.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10