- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

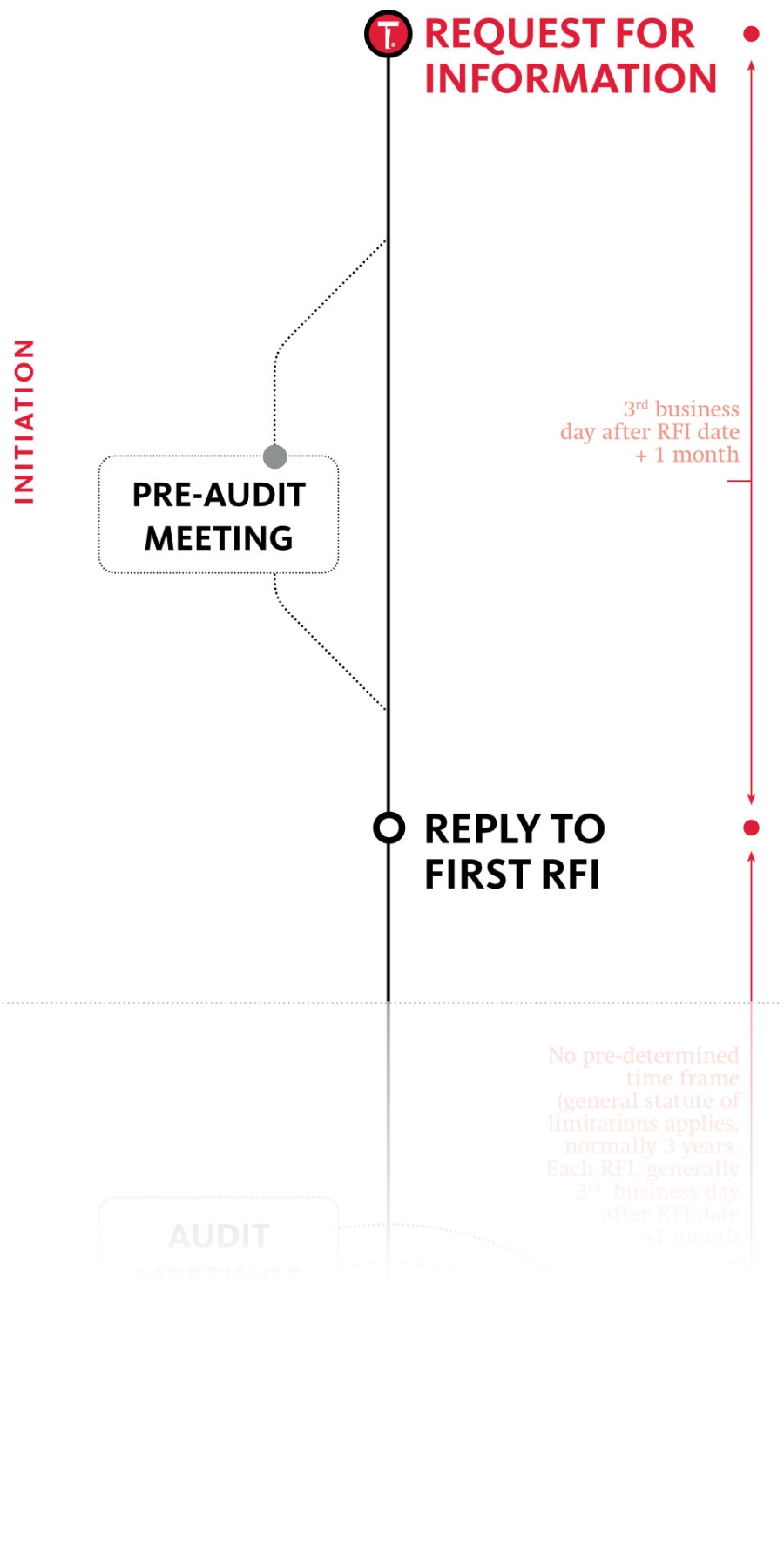

Click to enlarge

Bear in mind certain formalities and time constraints. Also, decide on the tone, style and level of detail of the reply, taking into account the rule of law.

Actually, applicable to any response to an RFI, the following formalities and timings are applicable:

In view of extent and nature of reply, we recommend the following:

- Before answering – notwithstanding the information might be available in the group – ask yourself: “Do I generally have access to the information requested at the level of the taxpayer specifically, and am I allowed to share it?” In case, as the specific taxpayer, you do not have access to the information and/or are not allowed to disseminate as such, one should inform the tax inspector of that in a correct and substantiated manner with reference to the legal provisions.

- In case, upon assessment, the question is not relevant, dare to question relevance, again in a substantiated manner taking into consideration the rules of law. Have the tax inspector explain the rationale of asking the question in such cases.

- Address the questions raised in a direct and concise manner – i.e. answer the question, nothing more, nothing less.

- As a taxpayer, keep your tone neutral and polite, yet determined to answer in sync with your obligations with due respect for your rights.

- In case when the request contains a question to motivate a certain tax filing position, first assess who has the burden of proof to determine the mode and extent of answering.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10