- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

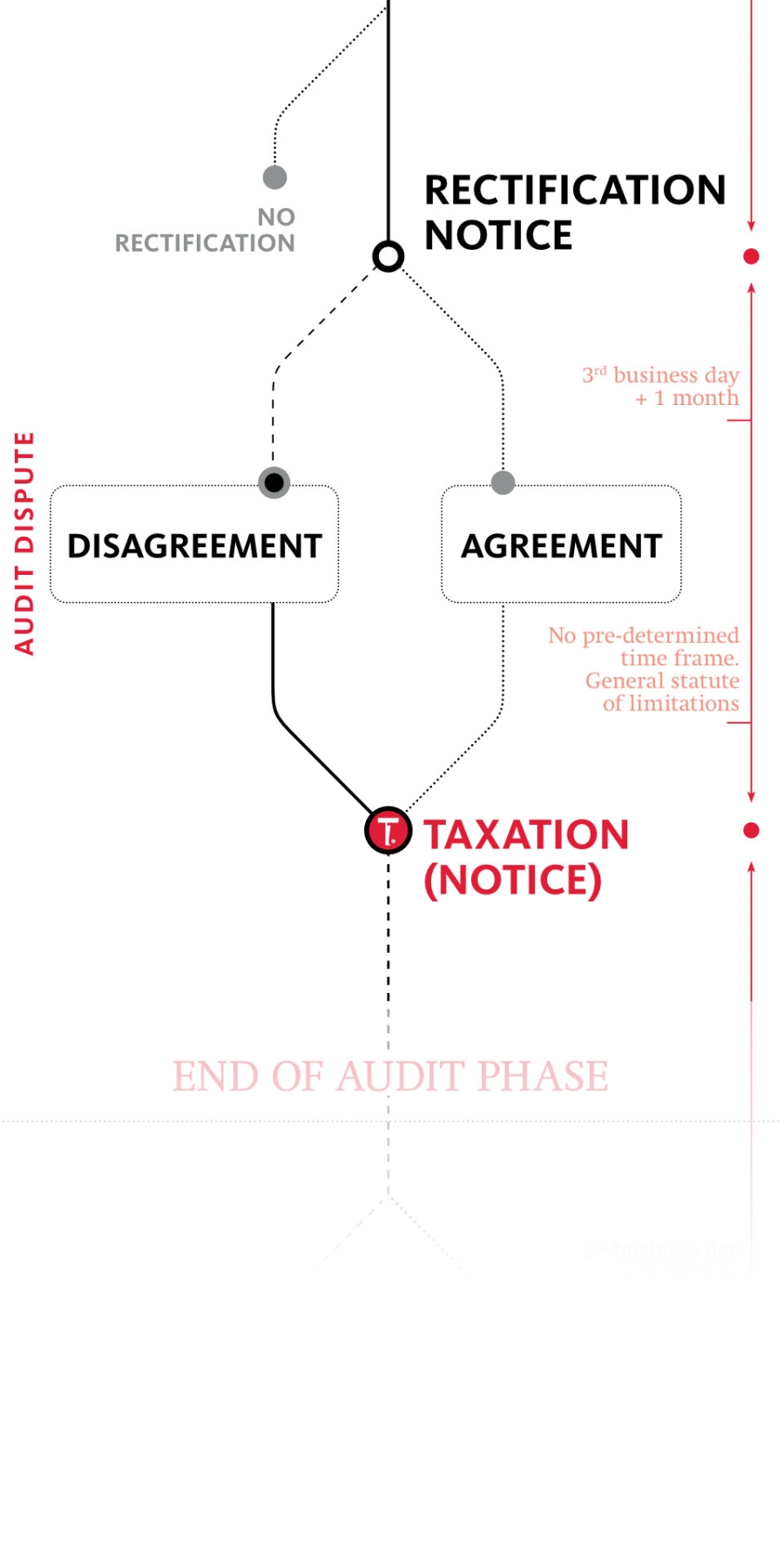

Almost simultaneously with the Rectification Notice a taxpayer will receive a Taxation Notice and the actual tax bill on the basis thereof. In the Taxation Notice the tax authorities state their (final) position on and argumentation for the additional taxes due by the taxpayer, including interests and penalties due. As such, the taxpayer becomes liable for these amounts due, and should primarily assess in detail the (altered) argumentation of the tax authorities (compared to the Rectification Notice, as a consequence of the arguments provided in the reply to the Rectification Notice).

Generally under the pain of nullity, only after the timeframe to reply to the Rectification Notice has elapsed, the tax authorities may send the taxpayer a Taxation Notice (“kennisgeving van beslissing tot taxatie” / “notification de la décision d’imposition”), containing the final position of potential additional taxation, and including a reply to the taxpayer’s arguments put forth in its reply to the Rectification Notice.

In many instances, this is largely a reprise of the argumentation of the Rectification Notice, but we have experienced cases where the tax authorities effectively substantially altered their position. In cases, where the Taxation Notice does not sufficiently motivate why taxpayer’s arguments have been neglected or even ignored, we are of the view that in the Administrative Claim, this should be highlighted, again in the light of bearing in mind building the taxpayer’s case for the potential further judicial procedure. We are confident that acting firmly and holistically from the beginning, and ultimately in the reply to the Rectification Notice in the end saves time and efforts to come to an acceptance of the original tax filing position or agreeable solution on the core issues at hand.

Subsequently, and automatically the reassessment is processed at the side of the Belgian tax authorities and the taxpayer receives their bill of Taxation (“aanslagbiljet” / “avertissement-extrait de role (note de calcul)”). This creates a legal debt obligation in the hands of the taxpayer (outstanding amount of tax due, interest and penalties).

In view of collecting taxes, it is worthwhile to notice that the disputed taxes are generally suspended upon explicit request to the competent tax receiver. On the other hand, it should be noted that taxes effectively paid, whilst disputed, attract interest that becomes payable by the Belgian government when the dispute is finally settled in the advantage of the taxpayer (cf. also Administrative Claim next).

Finally, it should be noted that the Belgian tax authorities can issue multiple reassessments, as deemed necessary and duly respecting the applicable statute of limitations. However, if they base an additional tax for a particular assessment year which is based on elements that have already been taxed in respect of another assessment year (as contained in a previous tax bill), the taxpayer has the right to also initiate (again) an administrative claim against the previous tax bill after the receipt of the additional tax bill.

With the receipt of the tax bill, the audit process comes to an end, and we enter into the administrative appeal phase.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10