- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

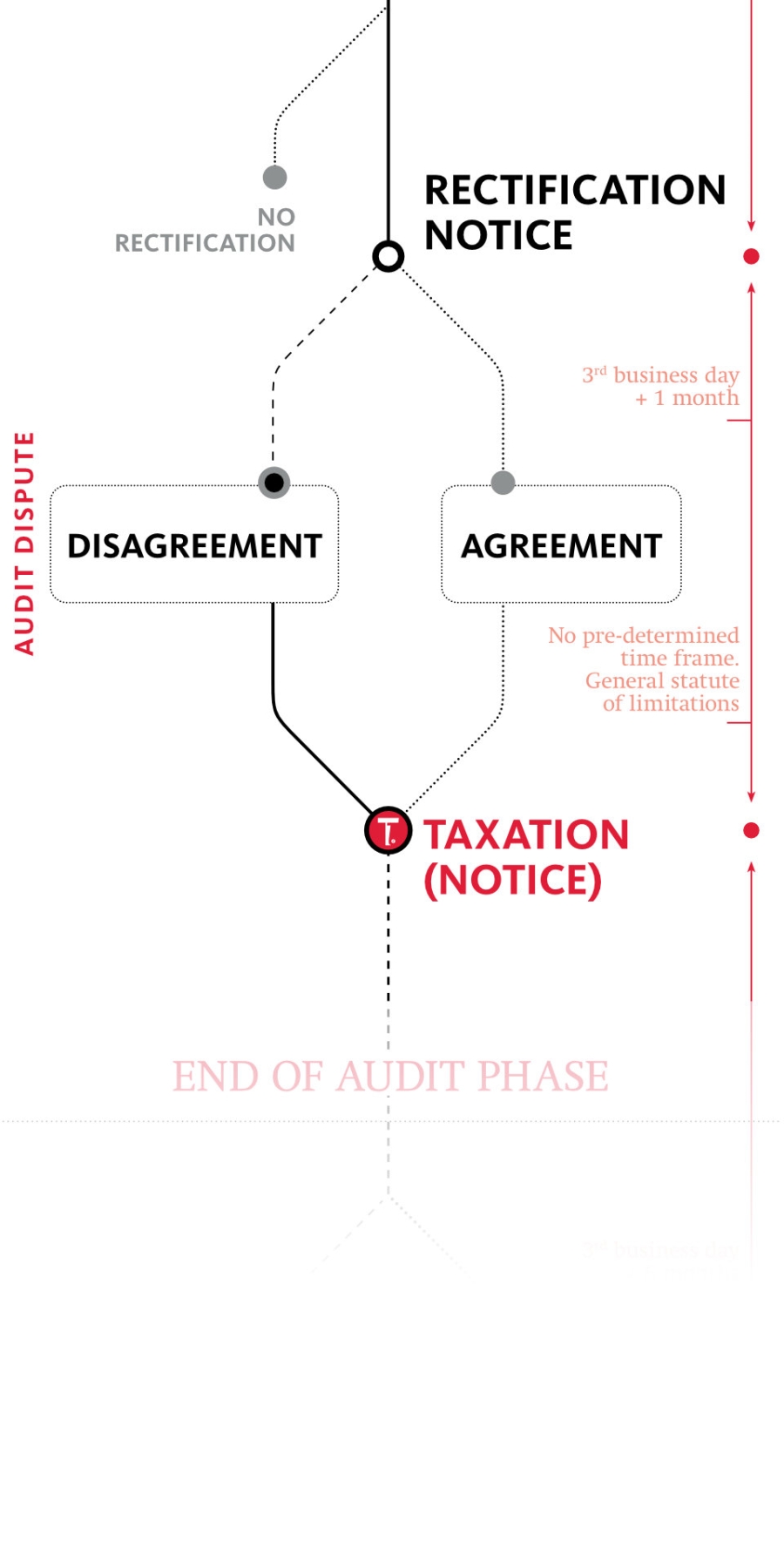

The Rectification Notice provides for a substantial formality for the tax authorities to start the tax procedure in view of imposing an additional taxation. In most instances, we advise taxpayers to motivate their disagreement substantially – although legally not required – both on the basis of the technical merits of the case, as well as bearing in mind already building their case for a potential juridical procedure. This way, striving for settlement in the administrative phase is not hampered by a fear of not having considered potential judicial outcomes in case of non-agreement.

At a certain point in time, at the end of the audit phase, the tax inspectors in charge of the audit will take their (final) position and if they feel that the tax return of the taxpayer is to be reassessed (whether or not agreement could have been established during the actual audit) they issue a Rectification Notice (“bericht van wijziging” / “avis de rectification”). In order to avoid nullity, this Rectification Notice is to be sent to the taxpayer by registered mail.

The Rectification Notice should explain in a sufficiently motivated manner the intent of the tax authorities to change the taxpayers filed tax return, based on their findings during the audit. In practice, the Rectification Notice is considered by the tax administration as an invitation to discuss the matters of disagreement, and to initiate further discussion and ‘negotiations’.

Taxpayers have 1 month to reply to the Rectification Notice, stating their agreement with the proposed changes or disagreement. This timeframe starts running from the 3rd business day following the date on which the Rectification Notice has been sent, and may be extended in case of legitimate reasons.

The key question to be addressed at this stage (supposing the taxpayer disagrees with the proposed changes): “Should I just state my disagreement, or support such disagreement with additional information and argumentation?”

Part of the answer is that a simple statement of disagreement formally suffices. Moreover, there are many instances in tax procedure that the reply to the Rectification Notice turned out to be a pro forma formality - an important one from a procedural perspective – not yielding any positive outcome in the position put forth in the Rectification Notice. As such, the Taxation Notice (“kennisgeving van beslissing tot taxatie” / “notification de la décision d’imposition”) follows swiftly including a copy/paste of the argumentation used in the Rectification Notice.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10